PPF - Comparative Advantage and Absolute Advantage: Videos & Practice Problems

Everyone has different levels of productivity. Who's better at making what? How do we define "better"?

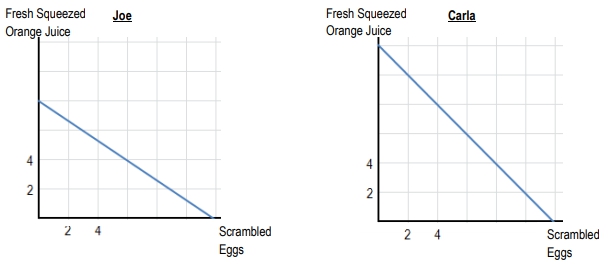

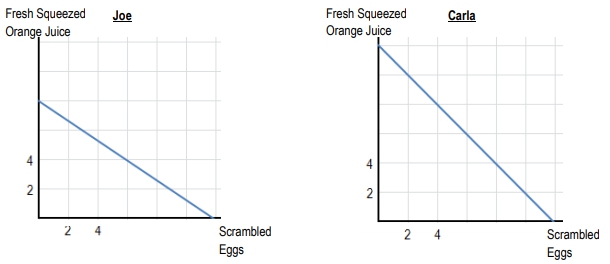

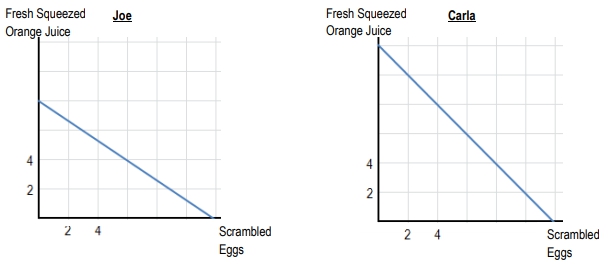

Who has the absolute advantage in making scrambled eggs?

Who has the absolute advantage in making fresh squeezed orange juice?

Who has the comparative advantage in making scrambled eggs?

Who has the comparative advantage in making fresh squeezed orange juice?

Do you want more practice?

Here’s what students ask on this topic:

Absolute advantage refers to the ability of an individual, firm, or country to produce more of a good or service with the same amount of resources compared to others. In contrast, comparative advantage focuses on producing goods or services at a lower opportunity cost. This means that even if one party has an absolute advantage in producing all goods, they can still benefit from trade by specializing in the goods for which they have a comparative advantage. This specialization and trade can lead to more efficient resource allocation and increased overall production.

To calculate opportunity cost, you need to determine the maximum output of two goods. For example, if you can produce either 20 gallons of hunch punch or 10 batches of pizza rolls, the opportunity cost of producing one batch of pizza rolls is the amount of hunch punch you give up. The formula is:

So, the opportunity cost of one pizza roll is 20/10 = 2 gallons of hunch punch. Conversely, the opportunity cost of one gallon of hunch punch is 10/20 = 0.5 pizza rolls.

Comparative advantage is crucial in trade because it allows for specialization, which leads to more efficient resource allocation and increased overall production. When individuals, firms, or countries specialize in producing goods for which they have a lower opportunity cost, they can trade to obtain other goods at a lower cost than if they produced everything themselves. This specialization and trade result in mutual benefits, higher productivity, and improved economic welfare for all parties involved.

No, a country cannot have a comparative advantage in producing all goods. Comparative advantage is based on the concept of opportunity cost. Even if a country has an absolute advantage in producing all goods, it will still have a lower opportunity cost for some goods compared to others. This means that it will have a comparative advantage in producing certain goods while other countries will have a comparative advantage in producing different goods. This difference in opportunity costs is what makes trade beneficial.

Specialization is the process of focusing on the production of a particular good or service in which an individual, firm, or country has a comparative advantage. By specializing, they can produce more efficiently and at a lower opportunity cost. This specialization allows for increased overall production and efficiency. When specialized producers trade with each other, they can obtain other goods at a lower cost than if they tried to produce everything themselves, leading to mutual benefits and higher economic welfare.