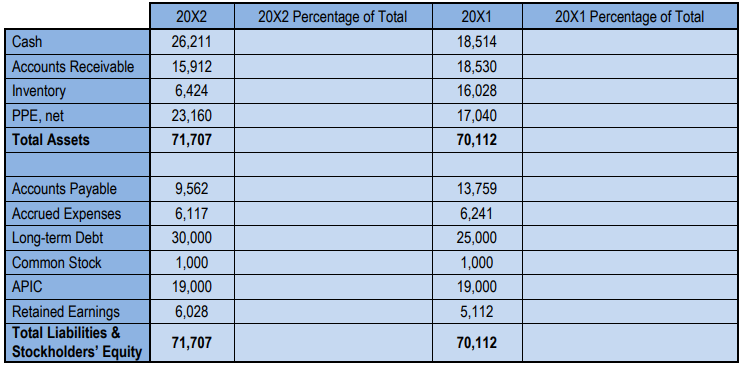

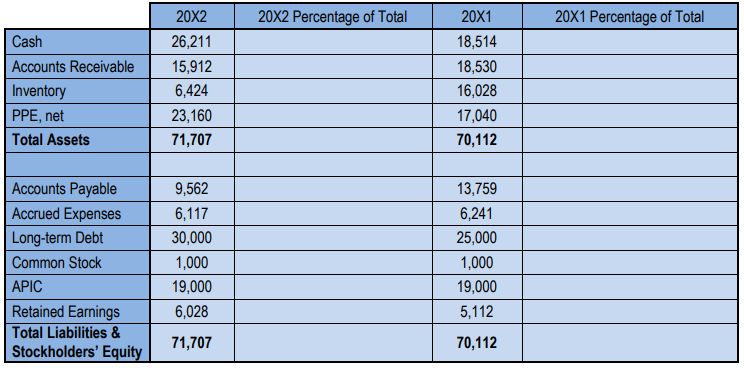

Understanding financial statements is crucial for effective financial analysis, and one key method for analyzing these statements is through vertical analysis. Unlike horizontal analysis, which examines percentage changes over time, vertical analysis focuses on expressing each line item as a percentage of a base amount within the same financial statement. This technique can be applied to both the income statement and the balance sheet.

For the income statement, the base amount is typically the net sales, which represents the total revenue generated from sales after deducting returns and allowances. In contrast, for the balance sheet, the base amount is total assets, while total liabilities and equity can also serve as the base since they are equal to total assets.

To perform vertical analysis, the line item amount is divided by the base amount, and the result is then multiplied by 100 to convert it into a percentage. For example, if the cost of goods sold is \$54,912 and net sales are \$65,455, the calculation would be:

Cost of Goods Sold Percentage = \(\frac{54,912}{65,455} \times 100 = 83.9\%\)

This percentage indicates that approximately 84% of net sales are used to cover the cost of goods sold. Similarly, gross profit can be calculated as a percentage of net sales, providing insight into profitability. For instance, if gross profit is \$10,543, the calculation would be:

Gross Profit Percentage = \(\frac{10,543}{65,455} \times 100 = 16.1\%\)

Continuing with this method, operating expenses can also be analyzed. For example, if selling expenses amount to \$2,411, the calculation would be:

Selling Expense Percentage = \(\frac{2,411}{65,455} \times 100 = 3.7\%\)

This analysis reveals how much of each dollar in sales is allocated to various expenses, ultimately leading to net income. For instance, if net income is \$3,120, the calculation would be:

Net Income Percentage = \(\frac{3,120}{65,455} \times 100 = 4.8\%\)

Through vertical analysis, stakeholders can gain valuable insights into the financial health of a business, understanding how revenues are distributed across expenses and profits. This method not only aids in internal decision-making but also enhances the ability to communicate financial performance to external parties.